Curious if foreigners can invest NISA Japan?

Starting in January 2024, the revamped NISA (Nippon Individual Savings Account) program allows all residents over 18—including foreign residents—to invest tax-free in Japan.

This guide is supervised by Yukako Yamazaki, a Certified Financial Planner® and founder of FP Office MIRAI.

About the Supervisor & Writer

Certified Financial Planner® / 1st Grade Certified Skilled Professional of Financial Planning

Founder of FP Office MIRAI (est. 2022)

Yukako Yamazaki is an experienced financial planner with a background as a registered customs specialist and bank teller. With her motto “Changing the future through reviewing the household budget,” she provides personal finance consultations, writes financial articles, and supervises financial books and publications.

Who This Article Is For

This article is for you if:

- You’re a foreign resident in Japan interested in building long-term savings

- You’re new to investing and want to explore tax-free options

- You’re uncertain about how NISA Japan applies to non-Japanese citizens

- You’re looking for a simple and reliable guide to the new 2024 NISA system

- You want to understand the pros and cons of NISA as a non-Japanese resident

Table of Contents

Chapter 1: Quick Video Guide

Chapter 2: How did NISA Japan start?

NISA stands for Nippon Individual Savings Account and was created based on the British ISA model.

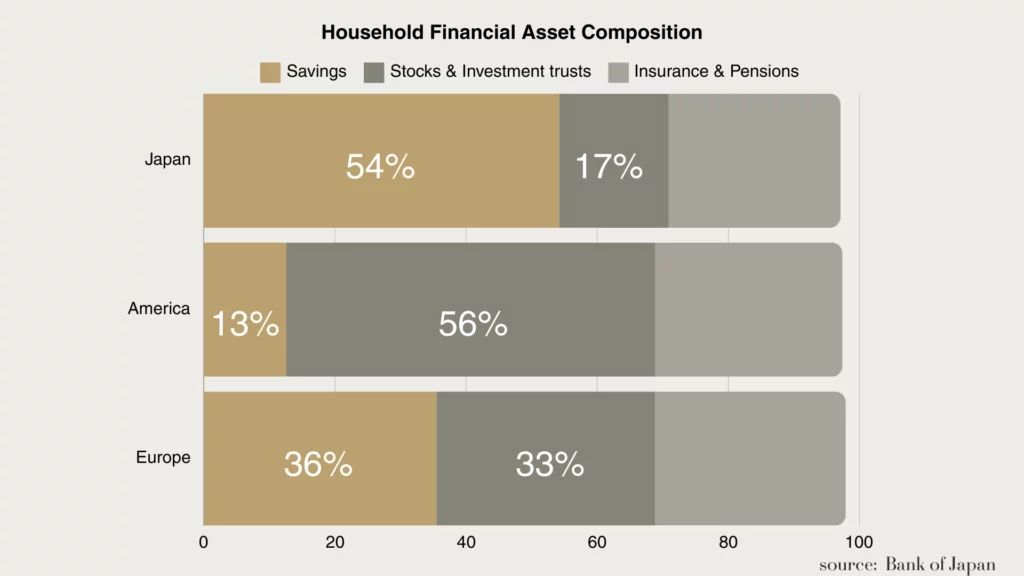

When looking at the breakdown of personal assets for Europeans and Americans, they tend to hold a higher percentage of investment products such as stocks and investment trusts, with a lower percentage in savings deposits. In contrast, for Japanese individuals, the ratio is reversed, with savings deposits accounting for half of their assets, as shown below.

Source: Bank of Japan, Flow of Funds

Japan is facing an aging population, and it is expected that public pensions will decrease in the future. In particular, the working generation is said to need to prepare for retirement funds through self-help efforts. It is known that with low interest rates on savings deposits, future funds may be insufficient.

Against this background, NISA was established by the government to encourage asset formation among the population. The original NISA, which began in 2014, ended at the end of 2023, and the new NISA, called Shin-Nisa, started on January 1, 2024. (Shin means New in Japanese)

Chapter 3: What is Shin-NISA (New NISA)?

NISA was restarted in January 2024 with expanded content. Here, I’ll explain the key features of the new NISA.

What is NISA Japan?

NISA, known as a tax exemption program for small investments by individuals, allows tax-free investments from small amounts, as the name suggests. In Japan, normally, investment profits are taxed at a rate of 20.315%. However, with NISA, investment profits are not taxed, allowing the full amount of gains to remain as profit.

For example, if you invest 1 million yen and it doubles to 2 million yen later, the tax would normally be 20% of the profit, which is 200,000 yen. However, with NISA, the entire profit of 1 million yen would be tax-free.

Not long ago, investing was seen as something only a few people did. However, with the introduction of NISA, it has become more accessible to the general public. NISA has expanded the base of investors, making it more widespread among the general population.

Related Post

What is the difference between Old NISA and New NISA?

The old NISA had a 5 or 20-year investment period and a limit of 6 or 8 million yen. Once sold, the investment space could not be reused, making the tax-free benefits limited.

In contrast, the new NISA expands the lifetime tax-free limit to 18 million yen and makes the tax-free holding period unlimited. This means you no longer need to worry about when you open the account or how long you invest. The limit is based on the purchase price and does not include capital gains.

For example;

- if you invest 1 million yen and it increases fivefold to 5 million yen

- the remaining investment limit is not 18 million yen – 5 million yen = 13 million yen, but 18 million yen – 1 million yen (purchase price) = 17 million yen.

Additionally, even if you sell stocks or mutual funds, the investment limit is restored based on the book value of the sold items and can be reused in subsequent years.

For example;

- if you invest 1 million yen and it increases fivefold to 5 million yen, the remaining investment limit is 18 million yen – 1 million yen (purchase price) = 17 million yen.

- If you sell the 5 million yen asset, the investment limit will return to 18 million yen the next year.

This allows for flexibility to cash out when needed and reinvest when you have more funds, making it easier to use according to your life events.

Investment Types

In the old NISA, you had to choose between Tsumitate NISA and General NISA. However, the new NISA has two categories within one system.

The new NISA has two categories: the “Tsumitate (Saving) Investment Limit” and the “Growth Investment Limit.”

- Tsumitate Investment Limit: Used for regular investments in mutual funds.

- Growth Investment Limit: Mainly used for stock investments.

| Japanese | Romaji | Hiragana | Definition |

|---|---|---|---|

|

つみたて投資枠 |

tsumitate toshiwaku |

つみたてとうしわく |

Regular Investment Limit |

|

成長投資枠 |

seicho toshiwaku |

せいちょうとうしわく |

Growth Investment Limit |

The new NISA

You can use both categories at the same time.

Source: Financial Services Agency

| Tsumitate / Regular Investment Limit | Seicho / Growth Investment Limit | |

|---|---|---|

|

Investment Method |

Regular Investment |

Lump-Sum Investment |

|

Investment Products |

Limited to Certain Investment Trusts that Meet Financial Services Agency Standards (Investment Trusts Suitable for Long-Term and Diversified Investment) |

Listed Stocks and Investment Trusts |

|

Tax-Free Holding Period |

Unlimited |

|

|

Account Opening Period |

Permanent |

|

|

Annual Investment Limit |

1.2 million yen |

2.4 million yen |

|

Tax-Free Holding Limit |

18 million yen (with 12 million yen within the Growth Investment Limit) |

|

Summary of the new NISA

Here’s a summary of the key points of the new NISA (Nippon Individual Savings Account):

Unlimited Tax-Free Holding Period:

You can continue tax-free investments for your entire life.

Combination of Tsumitate and Growth Investment Limits:

Allows for the simultaneous use of both investment categories, expanding investment options such as regular investment and stock investment, regular investment and investment trusts (lump-sum investment), regular investment only, and more.

- Lifetime Tax-Free Holding Limit of 18 Million Yen (Annual Limit of 3.6 Million Yen)

The annual limit for the Growth Investment Limit, which involves lump-sum purchases of stocks or investment trusts, is 2.4 million yen (holding limit of 12 million yen). For regular investments only, the annual limit is 3.6 million yen (holding limit of 18 million yen).

If you only do regular investments, you can also use the Growth Investment Limit of 2.4 million yen, making the annual limit 3.6 million yen. For example, you can use the full 3.6 million yen for regular investments with (Growth Investment Limit = 0 yen & Tsumitate Investment Limit = 3.6 million yen) or split it as (Growth Investment Limit = 2 million yen & Tsumitate Investment Limit = 1.6 million yen).

This means you can use the 18 million yen tax-free limit with regular investments alone. Conversely, the Growth Investment Limit cannot exceed 2.4 million yen per year, so the lifetime holding limit for the Growth Investment Limit is 2.4 million yen x 5 years = 12 million yen.

- Reusability of Tax-Free Investment Limits

If you sell stocks or investment trusts, the tax-free limit is restored by the amount of the book value (purchase price) of the sold items and can be reused in the following year.

Chapter 4: Can Foreign Residents in Japan Use the New NISA?

NISA is a system available to anyone residing in Japan who is 18 years or older.

Nationality does not matter; as long as you have a My Number card and identification documents with your address in Japan, you can open a NISA account.

The My Number is assigned to people who have a resident record in Japan, so foreign residents in Japan can also obtain a My Number card and use NISA.

Points to Note When Opening a NISA Japan Account

NISA accounts can be opened at financial institutions such as banks and securities companies. However, be aware that fees and the available investment products can vary between institutions.

| Bank | Securities firm | Internet Securities | |

|---|---|---|---|

|

Stock Investment |

✖ |

〇 |

〇

|

|

Number of Investment Trusts |

△

|

〇 |

◎ |

If you open a NISA Japan account at a bank, you can purchase investment trusts but not stocks. If you want to invest in stocks, you should open an account at a securities company.

The types and number of investment trusts available for purchase also vary by financial institution. Securities companies generally offer a wider range of investment trusts than banks. Among securities companies, internet securities firms typically offer more options than traditional securities companies with physical branches.

Internet securities firms also tend to have lower fees. However, purchase fees for regular NISA investments are free at any financial institution.

Since you can only have one NISA account, choose a financial institution that suits your investment style. However, you can change your financial institution once a year.

Related Post

Chapter 5: Benefits of Using the New NISA for Foreign Residents in Japan

Both Japanese and foreign residents in Japan can enjoy the same benefits from NISA.

- Tax-Free Profits from Investments (capital gains, dividends, distributions): Normally, profits from investments are taxed at a rate of 20.315%. For example, if you receive dividends of 10,000 yen from stock investments, 2,000 yen would be deducted as tax, leaving you with 8,000 yen in profit. However, with NISA, the full 10,000 yen in dividends would remain as profit.

- Unlimited Tax-Free Holding (Investment) Period: Future government policies could change, but with current policy, ax-Free Holding (Investment) Period is unlimited. The removal of the tax-free holding period limit allows you to start investing at a time that suits you.

- Freedom to Sell Investments Anytime: There are no restrictions on when you can sell stocks or investment trusts. You can sell them at any time, for any reason.

- Reusable Investment Limit: When you sell stocks or investment trusts, the tax-free limit is restored based on the book value of the sold items for the following year. You can use this restored limit to reinvest. You can reuse (reinvest) the tax-free holding limit of up to 18 million yen as many times as you like. You can use the 18 million yen investment limit for a lifetime, and the profits from it will always be tax-free.

Chapter6: Drawbacks of Using the New NISA for Foreign Residents in Japan

While NISA offers many benefits, it’s important to be aware of the drawbacks as well.

- Risk of Principal Loss: NISA allows for tax-free profits, but investing in stocks or investment trusts without principal protection means there’s no guarantee of making a profit.

- Inability to Offset Losses with Gains in Taxable Accounts: Losses in a NISA account cannot be offset against gains in taxable accounts. For example, If you have multiple accounts holding investment trusts, such as Account A (profit of 1 million yen) and Account B (loss of 2 million yen), when combined, you would have a net loss of 1 million yen. This loss is not taxable.

However, NISA accounts are tax-exempt, so you cannot offset the losses from other accounts against them. NISA only provides benefits when there are profits.

- Ineligibility for Foreign Tax Credit: Profits from investments in foreign stocks or ETFs in a NISA account are tax-free in Japan but taxable in the foreign country. Foreign tax credits to avoid double taxation are not applicable.

- Restrictions on Purchasing Certain Products: Some securities companies restrict the purchase of certain products, such as U.S. stocks or U.S. ETFs, for U.S. citizens, green card holders, or residents of the U.S.

- Ineligibility upon Moving Abroad: To use NISA, you must be a resident of Japan. Therefore, if a foreign resident moves abroad, they must cancel their NISA.

- Temporary Moves Abroad: Even if a Japanese person temporarily moves abroad, they must freeze or cancel their NISA account.

Chapter7: Who is New NISA Suitable For?

New NISA is a system where you can manage your assets tax-free with a limit of 18 million yen and no time limit. Regardless of nationality, as long as you reside in Japan, you can use NISA for asset formation.

NISA was created for long-term asset formation. It’s suitable for those who are not seeking immediate profits but can invest over a long period.

Since all investments involve risks and potential losses, it’s important to fully understand the mechanisms, advantages, and disadvantages of NISA before starting.

Even for foreign residents in Japan, self-help asset formation is essential for living in Japan in the medium to long term. Consider using NISA Japan as part of your financial planning.

Related Post

Chapter8: Frequently Asked Questions (FAQ) – NISA Japan

1. What is NISA and why was it created?

NISA (Nippon Individual Savings Account) is a tax-free investment program for individuals in Japan. It was created to encourage long-term asset formation, especially since Japanese households traditionally hold more savings than investments. The program is modeled after the British ISA system.

2. What is the difference between Old NISA and New NISA (Shin-NISA)?

The old NISA had limited investment periods (5–20 years) and caps (6–8 million yen), and sold investments could not be reinvested. The New NISA, launched in January 2024, has a lifetime tax-free limit of 18 million yen, unlimited holding periods, and allows reuse of investment limits after selling assets.

3. What types of investments are allowed under the New NISA?

The New NISA has two categories:

Tsumitate (Regular Investment) Limit: For mutual funds with long-term, diversified investment.

Growth Investment Limit: Mainly for stocks and other growth assets.

Both categories can be used simultaneously to expand investment options.

4. Can foreign residents in Japan use NISA?

Yes. Any resident aged 18 or older can open a NISA account, regardless of nationality. A My Number card and proof of residence in Japan are required. Foreign residents enjoy the same tax-free benefits as Japanese citizens.

5. What are the main benefits and risks of using NISA?

Benefits: Tax-free profits on dividends and capital gains, unlimited holding periods, freedom to sell anytime, and reusable investment limits.

Risks: Investment principal is not guaranteed, losses cannot offset taxable accounts, certain foreign stocks may be restricted, and NISA eligibility ends if you move abroad.

* This article is provided for general informational purposes only and does not constitute individual financial, tax, or legal advice. While reviewed and supervised by a certified financial professional, readers are encouraged to consult with their own financial advisor before making any investment decisions. Belonging JAPAN is not affiliated with or endorsed by any financial institution mentioned.