In Japan, gift tax — known as zōyozei (贈与税) — applies when someone receives money or property without compensation. There are two main systems: the annual taxation system and the settlement at inheritance system, both offering a basic exemption of 1.1 million yen. Generally, gift tax applies to all assets, including those located overseas. However, when a foreigner is involved — either as the giver or receiver — the rules become more complex.

This article, supervised by a certified financial expert, explains what foreign residents need to know about Japan’s gift tax and how to ensure proper tax compliance.

| English | Kanji | Romaji |

|---|---|---|

|

Gift Tax |

贈与税 |

Zōyozei |

Table of Contents

Profile of Writer

Representative of FP Office MIRAI;

Experienced as a Registered Customs Specialist, a bank teller, and transitioned to the path of a financial planner. Founded the financial planning office “FP Office MIRAI” in 2022.

With the motto “Changing the future through reviewing the household budget,” actively engages in household budget consultations, financial article writing, and book supervision, etc.

1st grade Certified Skilled Professional of Financial Planning, Certified Financial Planner®.

Chapter 1: How Gift Tax Works

In Japan, if you receive more than 1.1 million yen in gifts from individuals between January 1 and December 31 in a single year, you must pay gift tax (贈与税 / zōyozei). The first 1.1 million yen is exempt, but any amount above that threshold is taxable.

This exemption applies to the total amount received within the same year, regardless of how many people gave the gifts. For example, if a grandchild receives 1 million yen from a grandfather and another 1 million yen from a grandmother during the same year, the total gift is 2 million yen. In this case, 900,000 yen will be subject to gift tax.

Gift tax in Japan applies not only to cash but also to assets of value, including real estate, stocks, insurance payouts, cars, jewelry, and even golf club memberships. Essentially, any property or benefit with financial value can be taxed as a gift.

Chapter 2: Who Must Pay Gift Tax?

In Japan, the person receiving the gift—known as the recipient—is responsible for paying gift tax (贈与税 / zōyozei). The giver, or donor, does not pay this tax.

In principle, Japan’s gift tax applies to all assets, whether they are inside or outside Japan. However, when a foreign resident or someone living abroad is involved, the taxation rules change. Your tax obligation status determines whether you are taxed on global assets or only on assets located in Japan.

The Japanese tax system classifies individuals into two categories:

| English | Kanji | Romaji |

|---|---|---|

|

Unlimited tax obligor |

無制限納税義務者 |

Museigen nōzei gimusha |

|

Limited tax obligor |

制限納税義務者 |

Seigen nōzei gimusha |

1. Unlimited Tax Obligor

An unlimited tax obligor (無制限納税義務者 / Museigen Nōzei Gimusha) is someone who resides in Japan, regardless of nationality, or someone who lived in Japan within the past 10 years before receiving the gift.

Even if a person currently lives overseas, their relationship with the donor—for example, if the donor is a Japanese resident—may still qualify them as an unlimited tax obligor.

If you fall under this category, gift tax applies to all assets worldwide, not just those in Japan.

2. Limited Tax Obligor

A limited tax obligor (制限納税義務者 / Seigen Nōzei Gimusha), on the other hand, is only taxed on assets located in Japan. This status generally applies to foreigners who have lived in Japan for less than 10 years within the past 15 years and do not have close ties (such as family) with a Japanese resident donor.

Talk to a Financial Planner

Get clear answers in a free 20-minute online chat with a certified Financial Planner (English supported).

October 2025 — Limited to 10 spots!

Chapter 3: Do Foreigners Have to Pay Gift Tax?

Whether a foreigner must pay gift tax (贈与税 / zōyozei) in Japan depends on the nationality and residency status of both the donor (the person giving the gift) and the recipient (the person receiving it).

As explained earlier, Japan classifies taxpayers as either unlimited tax obligors or limited tax obligors.

If the recipient is an unlimited tax obligor, the tax applies to both domestic and overseas assets.

If the recipient is a limited tax obligor, only assets located in Japan are subject to gift tax.

This distinction is especially important for foreign residents, expatriates, and international families, as their global ties often affect their tax obligations.

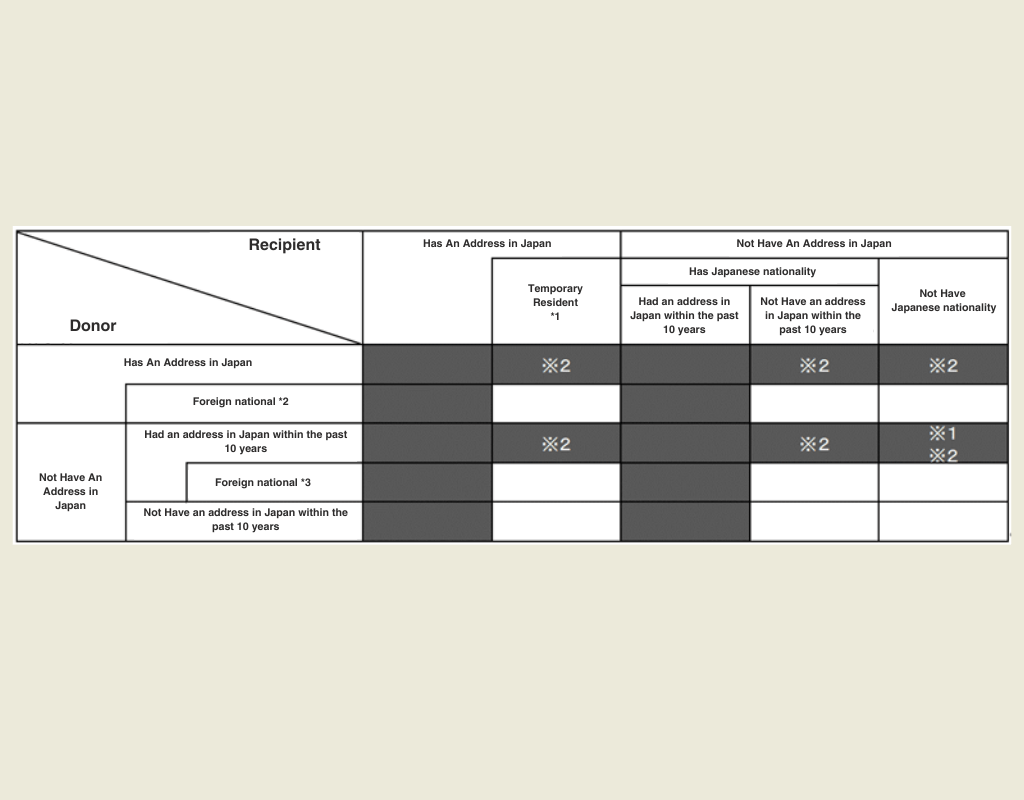

Scope of Taxable Assets Under the Gift Tax

The National Tax Agency (NTA) defines which assets are taxable under Japan’s gift tax system.

Black-shaded categories in the NTA chart represent unlimited tax obligors, meaning both domestic and foreign assets are taxable.

White-shaded categories represent limited tax obligors, meaning only assets in Japan are taxable.

Below is an overview of how these categories generally apply:

*1: A “temporary resident” refers to a person who, at the time of the gift, holds a residence status (as listed in the upper column of Appended Table 1 of the Immigration Control and Refugee Recognition Act; the same applies hereafter) and whose total period of residence in Japan within the 15 years prior to the gift is 10 years or less.

*2: Refers to a person who, at the time of the gift, holds a residence status and has a domicile (residence) in Japan.

*3: Refers to a donor who does not have a domicile in Japan at the time of the gift, but who had a domicile in Japan at some point within the 10 years prior to the gift, and who did not hold Japanese nationality at any of those times.

Source: National Tax Agency (NTA), “Gift Tax for Foreign Residents”

Cases Where Both Domestic and Foreign Assets Are Taxed (Unlimited Tax Obligors)

If you qualify as an unlimited tax obligor, gift tax applies to all assets, whether in Japan or overseas.

Typical cases include:

Both the donor and recipient live in Japan, including temporary residents.

(A temporary resident is someone with a residence status in Japan at the time of the gift and who has lived in Japan for a total of 10 years or less within the past 15 years.)Either the donor or recipient lives in Japan.

The donor or the recipient (if they have Japanese nationality) lived in Japan within the past 10 years.

The donor lived in Japan within the past 10 years, and gave assets to a non-Japanese recipient who does not currently live in Japan.

The donor is using the special tax deferral rule for exit taxation.

Cases Where Only Domestic Assets Are Taxed (Limited Tax Obligors)

If you qualify as a limited tax obligor, only assets located in Japan are subject to gift tax.

Typical cases include:

The donor is a foreign national (with a residence status, living in Japan), and the recipient is a temporary resident in Japan.

The donor is a foreign national (with residence status, living in Japan), and the recipient has Japanese nationality but has not lived in Japan at the time of the gift or within the past 10 years.

The donor is a foreign national (no Japanese nationality, not living in Japan at the time of the gift, but lived in Japan within the past 10 years), and the recipient has Japanese nationality but has not lived in Japan at the time of the gift or within the past 10 years.

The recipient does not have Japanese nationality.

Chapter 4: What Counts as a Gift and What Doesn’t

Besides receiving money or property directly, some forms of free financial support may also be treated as gifts for tax purposes. Below are examples of what the tax authority considers a gift, and what it does not.

Examples Treated as a Gift:

- Transferring the ownership of real estate or securities without a valid reason

- Receiving insurance money (life or damage insurance) without paying the premiums

- Having debt forgiven

- Buying real estate or other assets at a very low price

Examples Not Treated as a Gift:

Support for living expenses or education from legally responsible family members, like spouses or parents

Gifts from a company to an individual (these are taxed as income, not gift tax)

Seasonal gifts like summer/winter gift sets, congratulatory gifts, sympathy gifts, or funeral offerings

Chapter5: Important Things Foreigners Should Know About Japan’s Gift Tax

Understanding Japan’s gift tax (贈与税 / zōyozei) can be challenging—especially for foreigners who receive or give assets across borders. This chapter highlights key points that foreign residents and non-residents should pay attention to when handling gifts involving Japan.

Receiving a Gift from Abroad

When receiving a gift from overseas, the first step is to determine whether you are classified as an unlimited tax obligor (無制限納税義務者) or a limited tax obligor (制限納税義務者).

This classification depends on several factors:

Your residency status (whether you currently live in Japan)

Whether you have had a domestic address in Japan within the past 10 years

Your nationality

Your status determines which assets are subject to gift tax:

Unlimited tax obligor: All assets, both in Japan and overseas, are taxable.

Limited tax obligor: Only assets located in Japan are subject to gift tax.

It’s important to accurately determine your classification before accepting a large monetary gift or valuable property from abroad. Misunderstanding your tax status can lead to underreporting and potential penalties.

Tip from a Certified Financial Planner (CFP):

If you are unsure of your classification, consult a licensed tax professional or financial planner familiar with Japanese international taxation rules before accepting or declaring a gift.

Filing and Paying Gift Tax in Japan

If you need to file a gift tax return, the taxpayer (the recipient of the property) must submit the declaration and pay the tax between February 1 and March 15 of the year following the year in which the gift was made.

You can submit your tax return using e-Tax, by mail, or in person. Be careful not to miss the deadline or submit false information, as penalties such as late payment taxes or additional taxes may apply.

For payment, you can use convenience store payments, bank counter payments, or cashless options through smartphone apps.

If a foreigner who does not live in Japan is required to file a gift tax return, they must appoint a tax representative, select a tax payment location, and have the representative handle the process.

Chapter6: FAQ

1. Do foreigners have to pay gift tax in Japan?

Yes, foreigners may have to pay gift tax depending on their residency status, nationality, and where the assets are located. If you live in Japan or have lived here within the past 10 years, you may be classified as an unlimited tax obligor, meaning both domestic and overseas assets could be taxable.

2. How much can I receive as a gift in Japan without paying gift tax?

You can receive up to 1.1 million yen per year (January 1 to December 31) without paying gift tax. Any amount exceeding this threshold is taxable.

3. Who pays the gift tax in Japan—the giver or the receiver?

In Japan, the recipient (the person receiving the gift) is responsible for filing and paying the gift tax, not the giver.

4. What kind of assets are subject to gift tax?

Gift tax applies to money, real estate, stocks, vehicles, insurance proceeds, and other valuable property. However, regular living or educational support from family members is usually not taxable.

5. How and when should I file gift tax in Japan?

Gift tax returns must be filed between February 1 and March 15 of the year following the gift. Returns can be submitted through e-Tax, by mail, or in person at your local tax office.

6. What if I live outside Japan but receive a gift from someone in Japan?

In that case, you may need to appoint a tax representative in Japan to file and pay on your behalf. Whether you owe tax depends on your tax residency and the type of asset received.

7. Where can I get professional help with gift tax in Japan?

For personalized guidance, it’s best to consult a Certified Financial Planner (CFP) or licensed tax accountant familiar with Japan’s international taxation system.

Chapter7: Summary

Gift tax is generally a straightforward system, but it becomes more complex when foreigners are involved. In short, unless the gift is between foreign residents with temporary status or people who have lived abroad for over 10 years, the parties involved are classified as unlimited tax obligors. This means all assets, both in Japan and abroad, are subject to gift tax. However, there are exceptions, so it’s advisable to consult a professional to avoid errors or missed declarations when foreigners are involved in a gift.

*This article is for general informational purposes only and does not constitute individual financial, tax, or legal advice.

While the content is supervised by a Certified Financial Planner, readers are encouraged to verify current information with official government sources, banks, or licensed tax professionals.

Belonging JAPAN is not affiliated with any financial institution or government agency. Tax procedures, deadlines, and regulations are accurate as of October 2025 but are subject to change. Please confirm the latest details before filing.