If you are a foreign resident working in Japan and earn above a certain income, you may be required to file an income tax return in Japan. While the process in Japanese can seem daunting, understanding the basic system and key requirements will help you file and pay your taxes correctly. You can also complete the filing and payment online using a computer or smartphone, with manuals available in multiple languages, including English and Chinese.

In this article, Certified Financial Planner® Lili Katoh explains who needs to file an income tax return, the step-by-step process, and how it differs from the year-end tax adjustment.

Who This Article Is For

This guide is intended for foreign residents living and working in Japan who:

Earn income that may require filing a Japanese tax return.

Want to understand the difference between year-end tax adjustment and filing a tax return.

Are looking for clear, step-by-step instructions on how to calculate, submit, and pay their taxes.

Prefer practical advice with examples specific to company employees, freelancers, and non-employees.

Table of Contents

About the Supervisor & Writer

Certified Financial Planner®

Founder of Money Step Office Inc.

Lili Katoh specializes in insurance, life planning, and asset management. She is a Health Management Expert Advisor and author of “Setai Nenshū 1000 Man En” and “Gattsuri Tamaru Chokin Recipe”. Born in California, USA, she brings international insight to Japanese financial planning.

Chapter 1: What is an Income Tax Return in Japan?

In Japan, an income tax return (kakutei shinkoku) is the process of calculating your total income and the income tax you owe for the year, and reporting it to the tax office. It covers income earned from January 1 to December 31. You are responsible for working out your taxable income and the tax amount, then submitting the income tax return form to the tax office by the deadline. After filing, you pay the income tax based on the amount you declared.

If your income is above a certain level, you must file an income tax return in Japan. In most cases, this needs to be done between February 16 and March 15 of the year following the year the income was earned.

| English | Kanji | Romaji |

|---|---|---|

|

Income Tax Return |

確定申告 |

Kakutei Shinkoku |

Chapter 2: Do Foreign Residents Need to File an Income Tax Return in Japan?

To determine whether you need to file an income tax return in Japan, you first need to check if you are liable to pay Japanese income tax. Your tax liability depends on your residency status.

Foreign residents who are considered “residents” in Japan are, in principle, required to pay Japanese income tax on all income, regardless of where it is earned. In addition, there are categories such as “non-permanent resident” and “non-resident,” based on whether you have an address in Japan and how long you have lived here. Each category has different rules on which types of income are subject to taxation.

Tax Liability by Residency Status in Japan

| Residency Status | Conditions | Taxable Income Scope |

|---|---|---|

|

Resident |

• Has an address in Japan

• Has had a residence in Japan continuously for one year or more

※ Excludes non-permanent residents |

Worldwide income (all income including foreign-source income) |

|

Non-Permanent Resident |

• Meets the definition of “resident”

• Does not have Japanese nationality

• Has lived in Japan for a total of 5 years or less in the past 10 years |

All income except foreign-source income, plus foreign-source income that is paid in Japan or remitted to Japan |

|

Non-Resident |

• Does not meet the definition of “resident” or “non-permanent resident” (e.g., lives abroad) |

Japan-source income only (e.g., salary from work performed in Japan, compensation for services provided in Japan) |

Source: Compiled by the author based on the Immigration Services Agency of Japan’s “Guidebook for Living and Working”

Chapter3: Who Needs to File an Income Tax Return in Japan (Common Examples)

Even if your residency status means you are subject to Japanese income tax, not everyone is required to file an income tax return in Japan. Japanese income tax applies to ten categories of income, depending on the nature of the earnings. These include salary income, business income (such as profits from freelance or self-employed work), dividend and capital gains income (from investments like stocks or mutual funds), and real estate income (such as rental profits from property investments).

Whether you need to file an income tax return depends on factors such as your type of work, the sources of your income, and the total amount earned. If you are required to file, you must prepare your return yourself and pay the tax by the deadline. The tax office does not send a notice telling you whether you need to file or how much you owe, so it is your responsibility to determine your filing obligation and calculate the amount due.

For Company Employees

For most company employees, income tax is automatically deducted from their salary at the time of payment (withholding tax), and at the end of the year, a year-end adjustment is carried out (see Chapter 4). This process completes both the filing and payment of income tax, so employees whose only income is from salary generally do not need to file an income tax return in Japan.

However, even company employees must file an income tax return if they meet any of the following conditions:

Annual income exceeds 20 million yen.

Receive salaries from two or more employers, and the combined amount of salary income not covered by year-end adjustment plus any income other than salary or retirement income exceeds 200,000 yen.

Receive salary from only one employer, but have more than 200,000 yen in income from sources other than salary or retirement income (e.g., side jobs, online auctions, short-term rentals, profits from stocks or investment trusts — excluding profits from NISA or iDeCo).

Earn taxable income from business activities, stock trading, or other sources outside of salary, resulting in additional income tax owed after calculation.

Source: National Tax Agency, “Q&A on Income Tax Return — Filing Obligations for Salaried Employees”

For Non-Company Employees

Unlike company employees, non-company employees generally do not have income tax automatically withheld from their earnings. Therefore, they often need to file an income tax return themselves. Filing is typically required if you fall under any of the following categories:

You earn income above a certain threshold from self-employment, freelance work, or investments. This includes income from online auctions, short-term rentals, and profits from stocks or investment trusts. (Note: Profits from NISA or iDeCo accounts do not require filing.)

You received retirement benefits, but your employer did not withhold tax at the time of payment.

You earn rental income from leasing real estate properties (real estate income).

Chapter 4: The Difference Between Year-End Adjustment and Income Tax Return

For company employees, filing an income tax return is generally unnecessary if their employer has completed the year-end adjustment process.

What Is Year-End Adjustment?

Year-end adjustment is a system where the employer reconciles the income tax withheld from monthly salaries based on the employee’s total annual income and applicable deductions.

Each month, income tax is withheld (known as gensen chōshū) from your salary based on an estimated annual income. However, income tax calculations allow for various deductions—such as for dependents (spouse or family members), social insurance premiums (health insurance, national pension, welfare pension), life insurance premiums, and medical expenses—that can reduce the taxable income.

When these deductions affect the final tax amount, the employer adjusts the tax withheld in the last paycheck of the year to reflect the accurate tax liability. This adjustment process is called the year-end adjustment (nenmatsu chōsei).

If the tax owed is more than what was withheld, the difference is collected in the year-end paycheck.

If too much tax was withheld, the excess is refunded in the same paycheck.

After this adjustment, the employer issues a withholding tax statement (gensen chōshūhyō), which details:

The total salary paid during the year

The total income tax withheld

The deductions applied

Any tax balance or refund from the year-end adjustment

This statement is an important document for verifying income and tax details.

| English | Kanji | Romaji |

|---|---|---|

|

Year-End Adjustment |

年末調整 |

Nenmatsu Chōsei |

|

Withholding Tax |

源泉徴収 |

Gensen Chōshū |

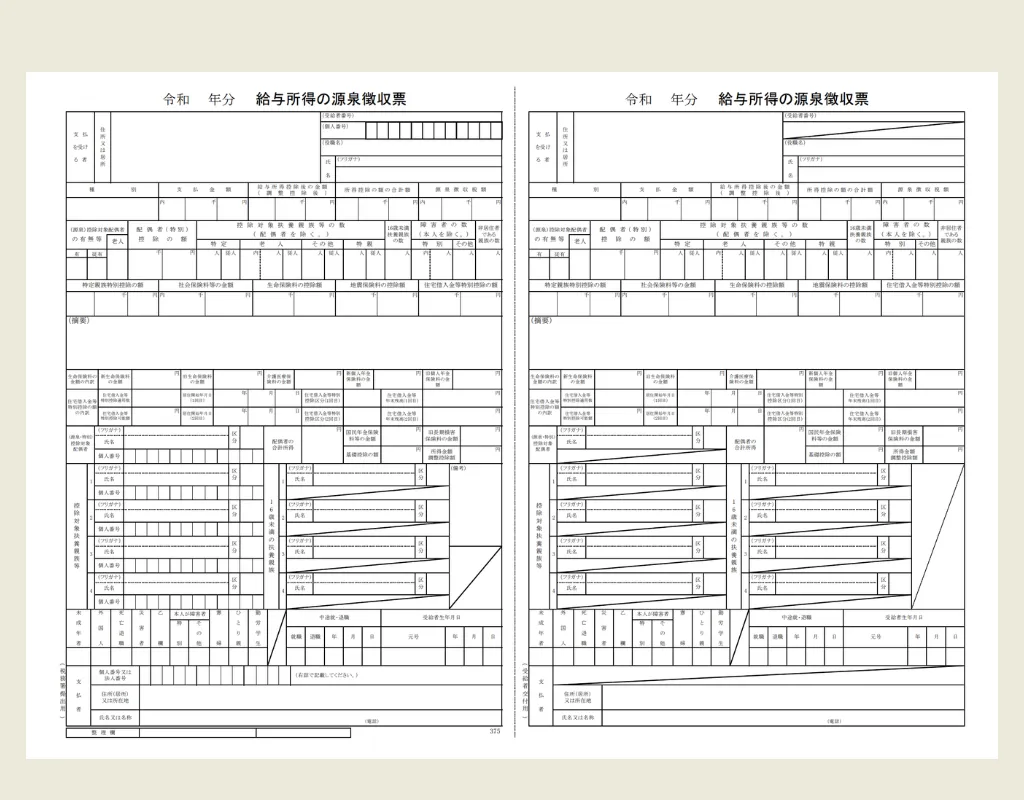

Example of withholding tax statement

Image Source:

National Tax Agency, “Tax Return Guide for Individuals” (PDF, 2023)

Year-end adjustment is handled by the employer, so employees themselves do not need to file any paperwork with the tax office to receive it. However, employees must submit certain documents to their workplace each year to help the employer complete the year-end adjustment. For example, the “Declaration of Exemptions for Dependents of Employment Income Earners” is used to report whether you have a spouse or family members you support. Additionally, if you have a life insurance policy in Japan, you need to provide the “Certificate of Insurance Premium Deduction” as proof.

Example of Dependent Exemption Declaration Form for Employees

Image Source:

National Tax Agency, “Tax Return Guide for Individuals” (PDF, 2025)

Filing a Tax Return Is Mainly for Non-Employees or Those Seeking Tax Refunds

A tax return (kakutei shinkoku) is a process where individuals calculate their own income and taxes and submit this information to the tax office. In principle, it is required for people who are not company employees and have a certain level of income (see Chapter 3 for details).

Even for company employees, filing a tax return is optional. If income tax has been overpaid through withholding, employees can file a tax return to claim a refund. This is particularly useful when applying specific deductions that cannot be claimed through year-end adjustment, allowing overpaid taxes to be reimbursed.

Common cases where a tax refund can be claimed through a tax return include:

Paying medical expenses and claiming the medical expense deduction

Making donations, such as through Furusato Nozei (hometown tax donations), and claiming the deduction for donations

Taking out a home loan and claiming the special deduction for housing loans (housing loan tax credit), applicable in the first year only

Chapter 5: Process for Filing a Tax Return

When filing a tax return, follow these steps:

1. Prepare the Necessary Documents

Gather all documents required for filing a tax return. Commonly required documents include:

Withholding slip (for company employees or other salary earners)

Documents to verify your My Number (Individual Number) (such as a My Number card or notification card)

Copy of your residence card (or alien registration certificate)

Proof documents for applying deductions (if claiming income deductions)

Examples: social insurance premium deduction certificates, medical expense receipts or statements, donation deduction certificates

Documents related to relatives or remittances (if you have dependents living abroad; Japanese translations may be required)

Bank account information for refunds (if claiming a refund; e.g., a copy of your bank passbook)

2. Calculating Income and Deductions

From your total income for the year, subtract necessary expenses and applicable income deductions—such as the basic deduction, social insurance premium deduction, life insurance premium deduction, medical expense deduction, and donation deduction. This calculation determines your taxable income and the amount of tax owed.

3. Preparing the Tax Return

Prepare your tax return by filling out the paper forms distributed at tax offices or by using the “Tax Return Preparation Corner” on the National Tax Agency’s website. Follow the on-screen instructions to complete your return online.

You can also use e-Tax, the electronic tax filing system, to complete both the preparation and submission of your tax return, as well as payment of taxes, entirely online.

4. Submitting the Tax Return

Once your tax return is prepared, you can submit it in one of the following ways:

In person at the tax office: Bring the completed tax return to the counter of your local tax office.

By mail: Send the tax return along with any required supporting documents to your local tax office or the submission processing center via postal mail or courier.

Online via e-Tax: Submit the tax return and supporting documents electronically through the National Tax Agency’s website. A My Number card may be required.

5. Payment or Refund

After completing your tax return, you may either need to pay additional tax or receive a refund:

Payment: If the calculation shows that you owe additional tax, it must be paid within the filing period.

Refund: If you have overpaid, the excess amount will be refunded to the bank account you specified.

The National Tax Agency provides detailed manuals on completing your tax return. You can refer to the official guides here:

English PDF – You can create a Final Tax Return at Home!

Simplified Chinese PDF – 可在自家进行确定申报!

Traditional Chinese PDF – 可在自家進行確定申告!

Vietnamese PDF – Có thể kê khai quyết toán tại nhà!

Portuguese PDF – Você pode fazer sua declaração de impostos em casa!

Nepali PDF – तपाईँ घरमा नै फाइनल ट्याक्स रिटर्न तयार पार्न सक्नुहुन्छ!

Chapter6: Filing Deadline for Income Tax Return in Japan

The filing period for an income tax return in Japan is generally from February 16 to March 15 of the year following the income year. If February 16 or March 15 falls on a weekend or national holiday, the deadline is extended to the next business day.

If you are required to pay taxes, both filing and payment must be completed within this period.

For taxpayers expecting a refund, you can submit your income tax return for the relevant period anytime within five years starting January 1 of the following year.

However, if you plan to leave Japan and no longer have a residence in the country, you must complete your income tax return and payment before departure. If filing or paying taxes after leaving Japan, you need to appoint a tax payment administrator in Japan and submit a “Notification of Tax Payment Administrator” to your local tax office. After departure, the appointed administrator will handle the filing and payment on your behalf.

Chapter7: Common Mistakes and Points to Note

Filing an income tax return in Japan requires careful attention to legal requirements and documentation. The following points highlight frequent mistakes and how to avoid them:

1. Failing to File on Time

If you are required to submit an income tax return, you must file and pay any taxes due within the official period. Missing the filing deadline, forgetting to submit, or filing late may result in additional taxes, penalties, or interest. The National Tax Agency (NTA) provides detailed guidance on penalties for late filing.

Official NTA guidance on penalties

2. Incomplete or Missing Documents

A complete income tax return requires more than just the form itself. You may need:

Withholding tax certificates (for employees)

Certificates for deductions such as insurance, medical expenses, or charitable contributions

Residence card or other identification

For deductions involving non-resident dependents or spouses, you must provide:

Proof of familial relationship

Remittance documentation for any financial support

Foreign-language documents must include a Japanese translation to be accepted.

3. Understanding Dependent Eligibility

Not all family members qualify for tax deductions. Rules for dependents were updated in 2023. Specifically, non-resident dependents aged 30–69 are not eligible unless one of these conditions is met:

The dependent has lost residence in Japan due to studying abroad.

The dependent has a recognized disability.

You provided ¥380,000 or more during the year for the dependent’s living or education expenses.

Source: Immigration Services Agency of Japan, “Tax” (PDF, n.d.)

Chapter8: Advice from a Financial Planner

If you live in Japan and have income, you may need to file an income tax return in Japan depending on your earnings and residency status. For most company employees, income tax is typically settled through year-end adjustments, so filing a tax return is not required. However, under certain conditions, filing an income tax return becomes necessary.

Even if you are not required to file, submitting a “refund claim” (還付申告) can be beneficial if you have overpaid taxes. It is recommended to check whether you qualify for deductions such as dependent exemptions, medical expense deductions, or charitable contribution deductions.

Since filing requirements and applicable deductions can vary depending on your employment type, income level, and family situation, consulting your local tax office or a certified tax professional specializing in taxation for foreign residents in Japan is highly advisable.

Chapter9: FAQ: Filing an Income Tax Return in Japan

1. Do all foreign residents in Japan need to file an income tax return?

Not necessarily. Your filing obligation depends on your residency status and income sources. Residents generally pay tax on worldwide income, while non-permanent residents and non-residents may have more limited obligations. Company employees may not need to file if all income is covered by year-end adjustment.

2. Can I file my income tax return online in English?

Yes. The National Tax Agency (NTA) provides e-Tax, an online filing system. Manuals and guidance are available in English and Chinese, allowing you to calculate, submit, and pay your taxes using a computer or smartphone.

3. What is the difference between year-end adjustment and a tax return?

Year-end adjustment is done by your employer to reconcile tax withheld from your salary. Filing a tax return (kakutei shinkoku) is done by the individual to report all income and claim deductions. Employees usually only need to file if they have additional income or want a refund.

4. What documents do I need to file an income tax return in Japan?

You typically need your withholding tax statement (gensen chōshūhyō), documents for deductions (like life insurance or medical expense receipts), and proof of other income if applicable. Non-employees may also need invoices or income records from freelance or business work.

5. What happens if I miss the filing deadline?

The deadline is usually March 15 for income earned the previous year. Late filing can result in penalties or interest on unpaid taxes. If you cannot meet the deadline, it’s important to contact the tax office as soon as possible to discuss extensions or arrangements.

Chapter10: Summary

Filing an income tax return in Japan involves calculating your total income and taxes for the year and submitting your declaration between February 16 and March 15 of the following year. It is essential to understand the required documents, the differences from year-end adjustments, and common points of caution to ensure accurate filing and timely payment. Whether you need to file depends on the type and amount of your income, as well as your working style. Multilingual guides are available to help foreign residents complete the procedure correctly, so make sure to review them as needed.

* This article is provided for general informational purposes only and does not constitute individual financial, tax, or legal advice. While reviewed and supervised by a certified financial professional, readers are encouraged to consult with their own financial advisor before making any investment decisions. Belonging JAPAN is not affiliated with or endorsed by any financial institution mentioned.