- October 1, 2025

- BELONGING JAPAN

iDeCo Japan (individual-type defined contribution pension) is a Japanese system that allows individuals to invest in financial products of their choice to build retirement savings. With Japan’s aging population and decreasing birthrate, many people feel that public pensions alone may not be sufficient for retirement. This guide is written by Yukako Yamazaki, Certified Financial Planner® (CFP®) and representative of FP Office MIRAI, with extensive experience in household budgeting, financial planning, and retirement advice.

This article explains eligibility, benefits, drawbacks, and practical tips for both residents and foreigners considering iDeCo in Japan.

Profile of Writer

Representative of FP Office MIRAI;

Experienced as a Registered Customs Specialist, a bank teller, and transitioned to the path of a financial planner. Founded the financial planning office “FP Office MIRAI” in 2022.

With the motto “Changing the future through reviewing the household budget,” actively engages in household budget consultations, financial article writing, and book supervision, etc.

1st grade Certified Skilled Professional of Financial Planning, Certified Financial Planner®.

Table of Contents

Chapter 1: What is iDeCo Japan?

iDeCo Japan is designed to supplement Japan’s public pension system. Participants contribute regularly and manage their own funds to grow their retirement assets.

Eligibility: You must be enrolled in the National Pension system.

Foreigners: Non-Japanese residents enrolled in the National Pension can also participate.

Investment Options: Mutual funds, time deposits, and insurance products.

Withdrawal: Assets cannot be withdrawn until age 60.

Why iDeCo Japan exists:

Japan’s public pension is pay-as-you-go: current workers’ contributions fund retirees. With an aging society, relying solely on public pensions is increasingly difficult. iDeCo encourages personal responsibility for retirement savings.

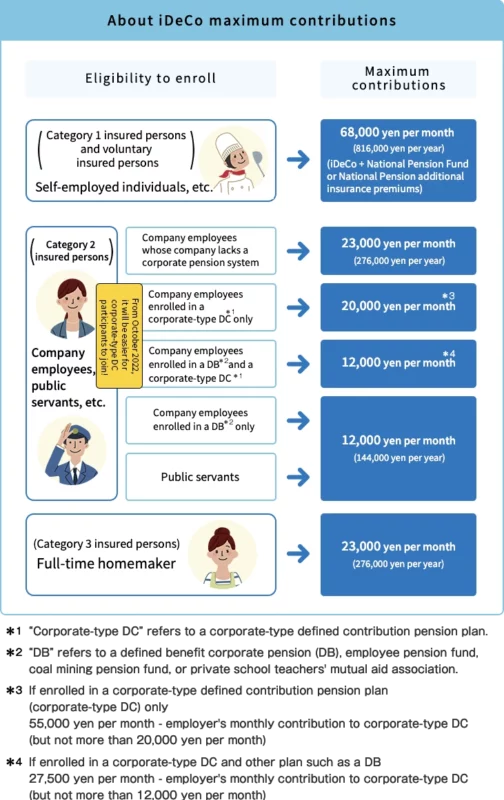

Chapter 2: iDeCo Japan Eligibility and Contributions

iDeCo Japan eligibility requires participation in the National Pension system.

| Category | Age Range | Notes |

|---|---|---|

|

National Pension subscribers |

20–59 |

Must reside in Japan |

|

Company employees & public servants |

60–64 |

Enrolled in corporate pensions (DC/DB) |

|

Voluntary National Pension enrollees |

60–64 |

Must not have completed 480 months of contributions |

|

Residents abroad |

20–64 |

Must remain enrolled in National Pension |

Contribution amounts for iDeCo Japan:

Start at 5,000 yen per month, in increments of 1,000 yen

Maximum contribution depends on employment category and other corporate pensions

Update 2025: Some contribution limits have increased starting December 2024

Photo and Source: National Pension Fund Association

Chapter3: Can Foreigners Join iDeCo?

iDeCo Japan allows foreign nationals aged 20–65 enrolled in the National Pension to participate. Those under 65 enrolled in Employees’ Pension Insurance are also eligible. Moving abroad and losing National Pension enrollment terminates eligibility.

Chapter 4: How to manage iDeCo?

Types of Investment Products

iDeCo Japan offers various investment products:

Variable investment trusts – Potential for higher returns but principal is not guaranteed.

Principal-guaranteed products – Time deposits and insurance, safer but lower returns.

Choosing a financial institution for iDeCo Japan: Options differ by bank or securities company. Check offerings before enrolling.

About Fees

The main fees for iDeCo that participants bear are as follows:

- Enrollment Fee (Initial Only): 2,829 yen (flat rate)

- Pension Benefit Fee (Per Benefit): 440 yen (flat rate)

- Management Fee (Monthly): 171 yen to over 500 yen

Fees 1 and 2 are the same regardless of the financial institution where you enroll in iDeCo. However, fee 3 varies by financial institution. The breakdown of the management fee is as follows:

- a. 105 yen per month (National Pension Fund Association)

- b. 66 yen per month (Outsourced administrative financial institution)

- c. 0 to approximately 500 yen per month (Account management fee paid to the contracted financial institution)

The combined total of fees a and b, 171 yen, is the same regardless of the financial institution. However, fee c varies depending on the securities company or bank you choose. Since account management fees are deducted from your contributions, higher fees can reduce your investment funds.

Given that fees can significantly impact investment efficiency over a long period, it is advisable to select a financial institution with lower fees.

Chapter 5: What is the benefit of iDeCo?

A. Tax Savings

You can reduce your income tax and resident tax by contributing to iDeCo. Contributions are fully deductible from your income, lowering your taxable income and, therefore, your taxes.

Here’s how the tax savings work if you contribute 20,000 yen per month for 20 years:

Contribution: 20,000 yen per month, 240,000 yen annually

For a 10% income tax rate:

- Income tax savings: 24,000 yen per year (240,000 yen × 10%)

- Resident tax savings: 24,000 yen per year (240,000 yen × 10%)

- Total annual savings: 48,000 yen

- Total savings over 20 years: 960,000 yen

For a 20% income tax rate:

- Income tax savings: 48,000 yen per year (240,000 yen × 20%)

- Resident tax savings: 24,000 yen per year (240,000 yen × 10%)

- Total annual savings: 72,000 yen

- Total savings over 20 years: 1,440,000 yen

Resident tax is always 10%, so savings are the same for everyone. However, higher income tax rates lead to more significant savings with iDeCo.

If you don’t pay income or resident taxes, you won’t benefit from these deductions.

B. Tax-Free Investment Gains and Reinvestment

Typically, investment gains are taxable, but with iDeCo, you don’t pay taxes on the profits. This means any gains from investments, such as dividends from mutual funds or interest from time deposits, are automatically reinvested tax-free.

For example, if you join iDeCo at age 40 and contribute 20,000 yen per month, with an average annual return of 3% from mutual funds until age 60, here’s how the tax savings would look:

|

Total Contributions (a) |

4,800,000 yen (20,000 yen × 12 months × 20 years) |

|

Investment Gains (b) |

1,753,211 yen |

|

Total Value (a + b) |

6,553,211 yen |

|

Tax Savings (b × 20.315%) |

356,164 yen |

Normally, you would pay around 356,000 yen in taxes on these gains. However, with iDeCo, you receive the full amount of 6,553,211 yen, including the 356,000 yen that would otherwise be taxed.

Note: The return on mutual funds is not guaranteed, so these numbers are for simulation purposes only.

C. Tax Benefits When Receiving iDeCo Assets

You can receive iDeCo assets in three ways:

- Lump Sum Payment

- As a Pension

- Combination of Lump Sum and Pension

Tax benefits are available when receiving these assets:

Lump Sum Payment:

When you take the entire amount as a lump sum, the retirement income deduction applies. This deduction is calculated separately from other income, with larger deductions for longer employment periods.As a Pension:

If you receive the amount as a pension, it is combined with other public or company pensions. You can apply the public pension deduction to this combined total.

D. Continue with iDeCo Even After Changing Jobs

You can transfer your pension assets between iDeCo, corporate-defined contribution pensions (corporate DC), and corporate-defined benefit pensions (DB).

So, even if you change jobs, you can carry over your iDeCo assets through the proper procedures. This portability ensures that your assets remain secure and manageable.

E. Lump-Sum Withdrawal from iDeCo

iDeCo typically does not allow early withdrawal once you join. Although you can stop contributing at any time, you must continue to manage your accumulated funds until you turn 60.

However, if you meet all the following conditions, you can receive a lump-sum withdrawal:

- Under 60 years old

- Not a participant in a corporate-defined contribution pension (corporate DC)

- Ineligible for iDeCo (e.g., exempt from national pension contributions, living abroad)

- Not a Japanese national living abroad (20 to 59 years old)

- Not receiving disability benefits from a defined contribution pension

- Have been enrolled in iDeCo and corporate DC for 5 years or less, or the balance of individual assets is 250,000 yen or less

- Within 2 years of losing eligibility for corporate DC or iDeCo

Chapter 6: What is disadvantage of iDeCo?

A. No Access to Funds Until Age 60

iDeCo is a pension system, so you cannot access your assets before age 60. Even after turning 60, you may not automatically start receiving benefits. If the total period of iDeCo and corporate DC contributions is less than 10 years, you will receive benefits at a later age, depending on your total contribution period:

- 8 to less than 10 years: Start at 61 years old

- 6 to less than 8 years: Start at 62 years old

- 4 to less than 6 years: Start at 63 years old

- 2 to less than 4 years: Start at 64 years old

- 1 month to less than 2 years: Start at 65 years old

Note that you cannot use iDeCo funds for purposes like housing or education.

B. Investment Risk and Variability

The value of your iDeCo assets can fluctuate depending on your investment choices.

For fixed deposits or insurance products: These choices do not risk losing your principal but might not yield significant growth. However, if the monthly management fees exceed the returns, your assets could decrease.

For mutual funds: They offer the potential for significant gains but come with the risk of losing your principal.

Decide whether you prefer stable returns or the potential for growth, and consider diversifying your investments. Regularly reviewing and adjusting your investment choices is important as you can change your investment options.

C. Considerations for Foreign Nationals Not Planning to Retire in Japan

iDeCo is a system where you generally cannot withdraw funds before age 60, and once you join, you cannot cancel early.

While iDeCo is beneficial for foreigners planning to spend their retirement in Japan, it may not be ideal for those who plan to move abroad in the future. You can only receive a lump-sum withdrawal if you meet all the conditions and have been enrolled for 5 years or less. Otherwise, you will have to wait until age 60 to access your funds.

D. Language Barriers

Understanding iDeCo involves navigating complex details such as choosing financial institutions, investment products, contribution limits, and eligibility age. Frequent system updates can make it challenging to stay informed, even for Japanese speakers. For foreigners who do not speak Japanese as their first language, the barriers to joining iDeCo may be higher.

Chapter7: Who Should Consider iDeCo?

iDeCo offers tax benefits and the potential to build substantial retirement savings through investment. It’s especially suitable for:

- Individuals who want to save for retirement in a disciplined manner

- Those looking to reduce their taxes (particularly beneficial for high-income earners)

- People who understand the system and are comfortable with investment risks

However, for foreigners, NISA might be a more flexible and user-friendly option for tax-free investing. It’s important to carefully evaluate whether iDeCo aligns with your needs and future plans.

Chapter8: FAQs – iDeCo Japan

Q1. What is iDeCo Japan?

A retirement savings system allowing individuals to invest in selected financial products with tax benefits.

Q2. Who can join iDeCo Japan?

Japanese residents and eligible foreigners enrolled in the National Pension system, aged 20–65.

Q3. Can I withdraw iDeCo Japan funds before 60?

Generally no. Only under strict conditions such as leaving Japan early or having minimal contributions.

Q4. What are the main benefits of iDeCo Japan?

Tax deductions on contributions

Tax-free investment gains

Portability between pension plans

Q5. Are there risks with iDeCo Japan?

Yes. Investments may fluctuate, fees reduce gains, and funds are inaccessible before retirement age.

Chapter9: Summary of iDeCo in Japan

Due to the accelerating aging population and declining birthrate, relying solely on public pensions for retirement will become increasingly difficult.

iDeCo is an excellent system that allows for tax savings while preparing retirement funds in a tax-free manner. While it lacks flexibility due to the principle that funds can only be accessed after age 60, this ensures that the assets are used solely for retirement.

Foreigners who are enrolled in the National Pension can also join iDeCo. However, if you plan to return to your home country in the future, you should consider joining carefully.

References; National Pension Fund Association

* This article is provided for general informational purposes only and does not constitute individual financial, tax, or legal advice. While the content has been reviewed and supervised by a certified financial professional, readers should confirm details with the relevant tax office or consult their own financial advisor before making decisions. Belonging JAPAN is an independent media platform and is not affiliated with or endorsed by any financial institution, government agency, or automobile association mentioned.