In Japanese, gift tax is called zōyozei, written as 贈与税 in Kanji. This tax applies when someone receives money or items for free from another person. Japan uses two systems for gift tax: the annual taxation system and the settlement at inheritance system. Both allow a basic exemption of 1.1 million yen. Normally, the tax covers all assets, even those outside Japan. But if a foreigner gives or receives the gift, the tax rules become more complicated. This article explains what foreigners need to know about gift tax in Japan.

| English | Kanji | Romaji |

|---|---|---|

|

Gift Tax |

贈与税 |

Zōyozei |

Table of Contents

Profile of Writer

Representative of FP Office MIRAI;

Experienced as a Registered Customs Specialist, a bank teller, and transitioned to the path of a financial planner. Founded the financial planning office “FP Office MIRAI” in 2022.

With the motto “Changing the future through reviewing the household budget,” actively engages in household budget consultations, financial article writing, and book supervision, etc.

1st grade Certified Skilled Professional of Financial Planning, Certified Financial Planner®.

If you’re interested in other articles about finance in Japan, such as NISA and taxes, you might find this article helpful.

Chapter 1: How Gift Tax Works

If someone receives more than 1.1 million yen in gifts from individuals between January 1 and December 31 in a single year, they must pay gift tax. The first 1.1 million yen is tax-free, but any amount over that gets taxed.

This 1.1 million yen limit applies to the total amount a person receives in a year. For example, if a grandchild receives 1 million yen from a grandfather and another 1 million yen from a grandmother in the same year, the total gift is 2 million yen. In this case, 900,000 yen will be subject to gift tax.

Gift tax doesn’t apply only to cash. It also covers things like real estate, stocks, insurance payouts, cars, and golf club memberships—almost anything of value.

Chapter 2: Who Must Pay Gift Tax?

The person who gives the gift is the donor, and the person who receives it is the recipient. In Japan, the recipient must pay the gift tax.

In most cases, gift tax applies to all assets, whether they are in Japan or overseas. However, when a foreign national or someone living outside Japan is involved, the rules change. The tax rules depend on whether the person is a unlimited tax obligor or a limited tax obligor. This status decides whether the tax applies to both domestic and foreign assets, or only to assets located in Japan.

| English | Kanji | Romaji |

|---|---|---|

|

Unlimited tax obligor |

無制限納税義務者 |

Museigen nōzei gimusha |

|

Limited tax obligor |

制限納税義務者 |

Seigen nōzei gimusha |

1. Unlimited Tax Obligor

An unlimited tax obligor is someone who lives in Japan, regardless of nationality, or someone who lived in Japan within the 10 years before receiving the gift. Even if a person hasn’t lived in Japan in the past 10 years, their relationship with the donor can still make them an unlimited tax obligor.

When an unlimited tax obligor receives a gift, gift tax applies to all assets—both in Japan and overseas.

2. Limited Tax Obligor

A limited tax obligor (Seigen Nōzei Gimusha) only pays gift tax on assets located in Japan.

More details will be explained later.

Chapter 3: Do Foreigners Have to Pay Gift Tax?

As explained earlier, whether a foreigner must pay gift tax depends on the nationality and residence status of both the donor (the person giving the gift) and the recipient (the person receiving the gift).

If the situation makes the recipient an unlimited tax obligor, gift tax applies to both domestic and foreign assets. If the recipient is a limited tax obligor, only assets located in Japan are subject to gift tax.

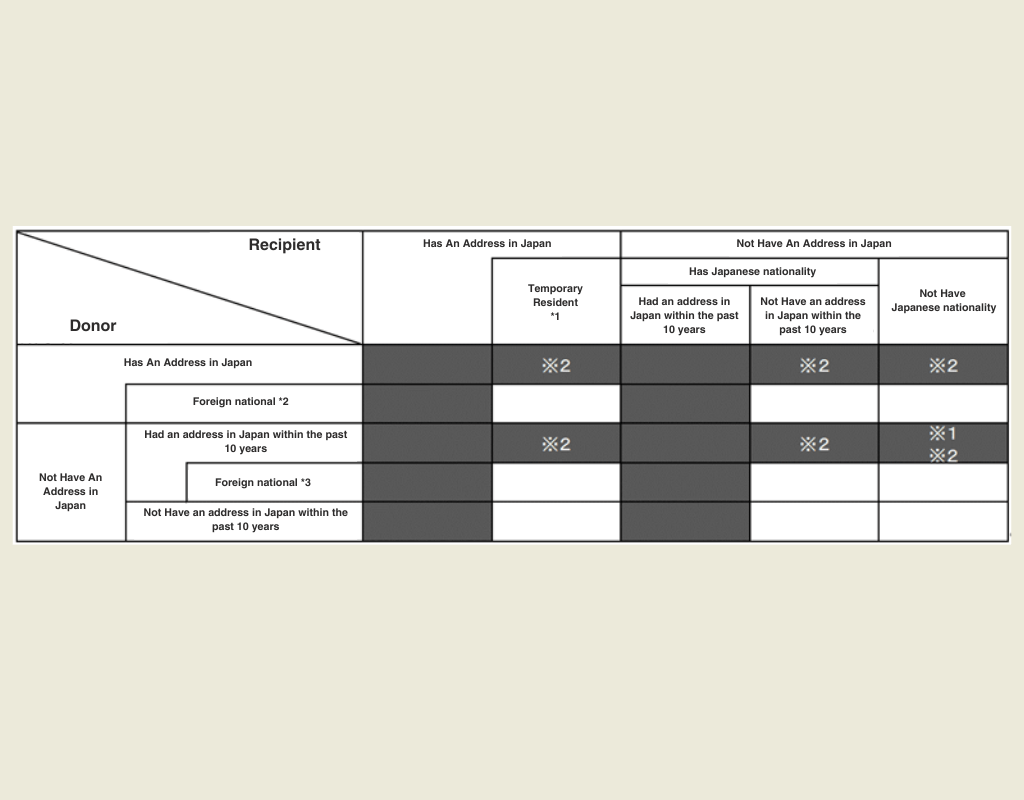

Scope of Taxable Assets Under the Gift Tax

The chart below comes from the National Tax Agency’s website and shows which assets are subject to gift tax.

If the recipient falls under a black-shaded category, they are considered an unlimited tax obligor.

If the recipient falls under a white-shaded category, they are a limited tax obligor.

Cases Where Both Domestic and Foreign Assets Are Taxed (Unlimited Tax Obligors)

If you qualify as an unlimited tax obligor, gift tax applies to all assets, whether in Japan or overseas.

Typical cases include:

Both the donor and recipient live in Japan, including temporary residents.

(A temporary resident is someone with a residence status in Japan at the time of the gift and who has lived in Japan for a total of 10 years or less within the past 15 years.)Either the donor or recipient lives in Japan.

The donor or the recipient (if they have Japanese nationality) lived in Japan within the past 10 years.

The donor lived in Japan within the past 10 years, and gave assets to a non-Japanese recipient who does not currently live in Japan.

The donor is using the special tax deferral rule for exit taxation.

Cases Where Only Domestic Assets Are Taxed (Limited Tax Obligors)

If you qualify as a limited tax obligor, only assets located in Japan are subject to gift tax.

Typical cases include:

The donor is a foreign national (with a residence status, living in Japan), and the recipient is a temporary resident in Japan.

The donor is a foreign national (with residence status, living in Japan), and the recipient has Japanese nationality but has not lived in Japan at the time of the gift or within the past 10 years.

The donor is a foreign national (no Japanese nationality, not living in Japan at the time of the gift, but lived in Japan within the past 10 years), and the recipient has Japanese nationality but has not lived in Japan at the time of the gift or within the past 10 years.

The recipient does not have Japanese nationality.

Chapter 4: What Counts as a Gift and What Doesn’t

Besides receiving money or property directly, some forms of free financial support may also be treated as gifts for tax purposes. Below are examples of what the tax authority considers a gift, and what it does not.

Examples Treated as a Gift:

- Transferring the ownership of real estate or securities without a valid reason

- Receiving insurance money (life or damage insurance) without paying the premiums

- Having debt forgiven

- Buying real estate or other assets at a very low price

Examples Not Treated as a Gift:

Support for living expenses or education from legally responsible family members, like spouses or parents

Gifts from a company to an individual (these are taxed as income, not gift tax)

Seasonal gifts like summer/winter gift sets, congratulatory gifts, sympathy gifts, or funeral offerings

Chapter5: Things Foreigners Should Be Careful

Things to Keep in Mind When Receiving a Gift from Abroad

When you receive a gift from overseas, you must determine whether you are an unlimited tax obligor or a limited tax obligor. This depends on the combination of the donor and recipient’s “residency status,” whether they have had a domestic address in the past 10 years, and their “nationality.”

You also need to know whether the gift is located in Japan or abroad. If you are an unlimited tax obligor, all your assets, both in Japan and overseas, will face gift tax. If you are a limited tax obligor, only your assets in Japan will face tax.

Things to Keep in Mind When Paying Gift Tax in Japan

If you need to file a gift tax return, the taxpayer (the recipient of the property) must submit the declaration and pay the tax between February 1 and March 15 of the year following the year in which the gift was made.

You can submit your tax return using e-Tax, by mail, or in person. Be careful not to miss the deadline or submit false information, as penalties such as late payment taxes or additional taxes may apply.

For payment, you can use convenience store payments, bank counter payments, or cashless options through smartphone apps.

If a foreigner who does not live in Japan is required to file a gift tax return, they must appoint a tax representative, select a tax payment location, and have the representative handle the process.

Chapter6: Summary

Gift tax is generally a straightforward system, but it becomes more complex when foreigners are involved. In short, unless the gift is between foreign residents with temporary status or people who have lived abroad for over 10 years, the parties involved are classified as unlimited tax obligors. This means all assets, both in Japan and abroad, are subject to gift tax. However, there are exceptions, so it’s advisable to consult a professional to avoid errors or missed declarations when foreigners are involved in a gift.

References

Source: National Tax Agency JAPAN

Source: National Tax Agency JAPAN

Source: National Tax Agency JAPAN